If you run finance for a mid-market company with operations in more than one country, your 2025 and 2026 audit cycles have probably surfaced at least one of these conversations: how to handle unrealized foreign exchange gains and losses consistently across subsidiaries, what the new International Financial Reporting Standard (IFRS) 18 presentation requirements mean for your income statement, whether your transfer pricing documentation would survive scrutiny, or whether Pillar Two minimum tax applies to your group yet.

This guide covers the five issues consuming the most CFO attention right now, and how the operational architecture behind international accounting needs to evolve to keep up.

For the technical detail on how multi-entity, multi-currency consolidation works in a cloud ERP, see our companion guide, NetSuite OneWorld: Multi-Entity and Multi-Currency ERP Guide. For financial planning and budgeting across subsidiaries, see NetSuite Planning and Budgeting (NSPB): Complete Guide to Financial Planning.

Change | Status as of 2026 | Who It Affects | Key Deadline |

|---|---|---|---|

IFRS 18: Presentation and Disclosure in Financial Statements | Issued by the International Accounting Standards Board (IASB) in April 2024. Effective for annual periods beginning on or after January 1, 2027. Early adoption permitted. | Any entity reporting under IFRS | January 1, 2027 (with comparative restatement) |

BEPS 2.0 Pillar Two: Global minimum 15% corporate tax | In active rollout. Enacted in most European Union (EU) member states, the United Kingdom (UK), Japan, South Korea, Canada, Australia, and others. The United States (US) has not enacted Pillar Two in full. Coverage is uneven globally. | Multinational groups with consolidated revenue above EUR 750 million. Smaller groups may be affected indirectly through top-up tax mechanisms in jurisdictions that have enacted it. | Varies by jurisdiction. Most early adopters effective from January 1, 2024 or 2025. |

Transfer pricing documentation (BEPS Action 13) | Local File, Master File, and Country-by-Country Report (CbCR) requirements now standard in most Organisation for Economic Co-operation and Development (OECD) and G20 jurisdictions. Enforcement is tightening. | Any group with related-party cross-border transactions | Ongoing. Filing deadlines vary by jurisdiction. |

Multi-currency volatility | Structurally elevated. Major emerging market currencies have seen sustained volatility against the US dollar and euro since 2022. | Any company transacting or reporting in multiple currencies | Continuous |

Evolving local tax regimes | Digital services taxes, withholding tax changes, e-invoicing mandates rolling out in Southeast Asia, Africa, Latin America | Companies with operations or sales in these regions | Varies by country |

This is the landscape CFOs are navigating in 2026. The five issues below are where it hits the finance function hardest.

Foreign exchange volatility has been structurally elevated since 2022, and the operational cost of handling it well has gone up with it.

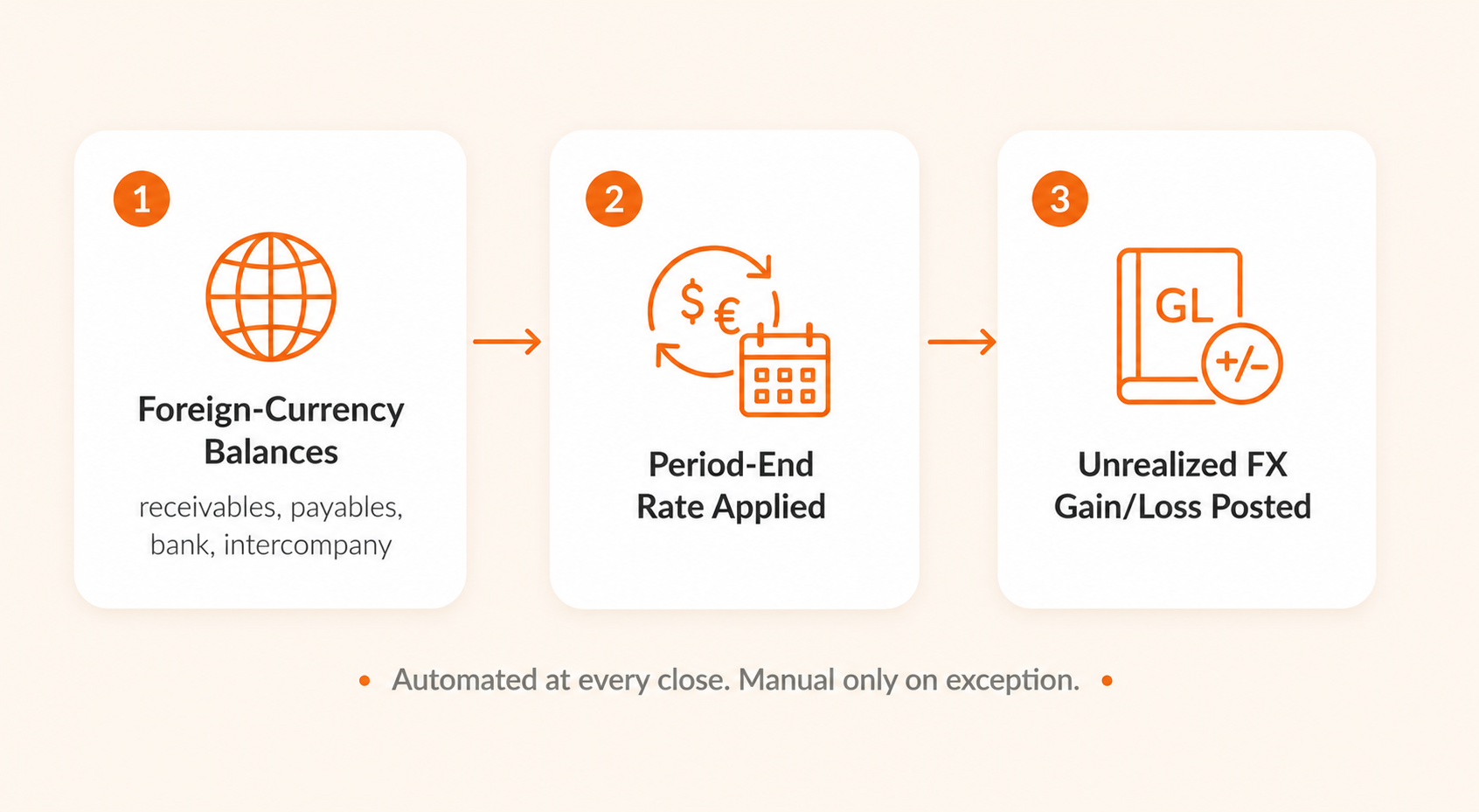

At every period close, finance teams have to restate foreign-currency balances (receivables, payables, bank accounts, intercompany) at the closing exchange rate. The unrealized gain or loss hits the income statement. When rates have moved hard within the period, that line item can swing reported earnings noticeably, and someone has to be able to explain it to the board.

The operational challenge for mid-market companies: revaluation needs to happen consistently across every subsidiary, using the same rate source and the same methodology, at the same point in the close cycle. When subsidiaries run on disconnected systems, the revaluation is manual, the timing drifts, and the consolidation picks up inconsistent results.

A pattern we see in multi-country implementations: the most common architecture for handling this cleanly is a single cloud ERP with automated exchange rate feeds, automated period-end revaluation, and separate General Ledger (GL) accounts for unrealized versus realized foreign exchange gains and losses. The revaluation posts automatically. The CFO reviews the impact rather than reconstructing it.

A pattern we see in multi-country implementations: the most common architecture for handling this cleanly is a single cloud ERP with automated exchange rate feeds, automated period-end revaluation, and separate General Ledger (GL) accounts for unrealized versus realized foreign exchange gains and losses. The revaluation posts automatically. The CFO reviews the impact rather than reconstructing it.

For companies with operations in volatile-currency markets (Africa, Southeast Asia, Latin America), the revaluation impact can swing quarterly earnings by 5 to 15 percent. This is not a rounding error. It is a board-level conversation, and the finance team needs to be able to produce the analysis quickly and consistently.

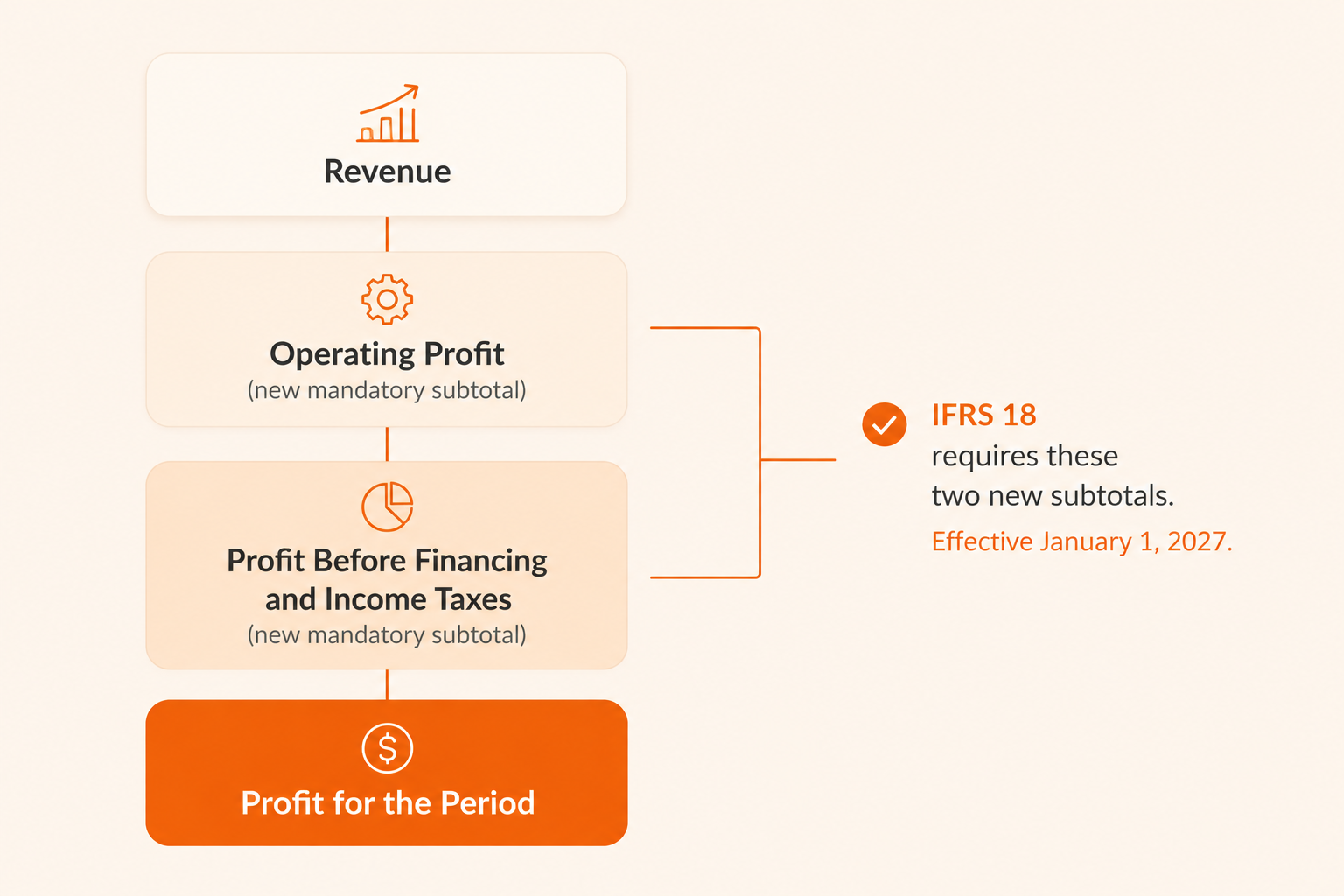

IFRS 18 lands in 2027 and changes how the income statement looks. The biggest practical shift: two new required subtotals (operating profit, and profit before financing and income taxes), tighter rules on how non-IFRS measures like adjusted EBITDA are disclosed, and a different way of classifying income and expenses. Comparative restatement is required, which means your 2026 numbers will need to be redone the year you adopt.

For mid-market CFOs reporting under IFRS, the practical impact is:

New income statement structure. The chart of accounts and reporting logic may need to be restructured to produce the required subtotals. Companies that currently use a highly customized income statement format will need to map their existing structure to the new requirements.

Management-defined performance measures. If you report adjusted Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA), adjusted operating profit, or other non-IFRS measures in your financial statements, IFRS 18 requires specific disclosure and reconciliation to the IFRS-defined subtotals.

Comparative restatement. The standard requires comparative period restatement, which means your 2026 financials will need to be restated when you adopt IFRS 18 for 2027 reporting.

The operational implication: your ERP's chart of accounts and financial reporting structure needs to be reviewed now, not in Q4 2027. For companies on a cloud ERP with a centralized chart of accounts, the adjustment is configuration work. For companies running disconnected accounting systems across subsidiaries, the mapping exercise is substantially harder.

A pattern we see: IFRS-compliant implementations that use a centralized, group-level chart of accounts with subsidiary-level segmentation (departments, classes, locations) can adapt to IFRS 18 through reporting-layer changes rather than a chart of accounts rebuild. Companies that allowed each subsidiary to build its own chart of accounts face a consolidation and remapping project first.

Pillar Two sets a minimum 15 percent effective tax rate for large multinational groups. Adoption is real but uneven. Most EU countries, the UK, Japan, South Korea, Canada, and Australia have enacted it. The US has not, though the Corporate Alternative Minimum Tax (CAMT) covers some of the same ground. The framework is part of the OECD's Base Erosion and Profit Shifting (BEPS) 2.0 work, formally known as the Global Anti-Base Erosion (GloBE) Rules.

For mid-market CFOs, the direct and indirect implications:

Direct applicability. Pillar Two applies to groups with consolidated revenue above EUR 750 million. Most mid-market companies fall below this threshold. However, mid-market subsidiaries of larger groups may be in scope through the parent's consolidated revenue.

Indirect pressure. Jurisdictions enacting Pillar Two may also tighten domestic tax rules for companies below the threshold, particularly around transfer pricing and incentive eligibility. The direction of travel is toward higher effective tax rates and more documentation.

Top-up tax mechanisms. Some jurisdictions have introduced Qualified Domestic Minimum Top-up Taxes (QDMTT) that apply to domestic entities regardless of group size. Monitor your jurisdictions individually.

The operational challenge: even if Pillar Two does not directly apply to your group, the data infrastructure required to evaluate your position (effective tax rate by jurisdiction, permanent differences, timing differences, deferred tax asset utilization) is the same data infrastructure you need for strong multi-jurisdictional tax compliance generally. Building it for Pillar Two readiness improves your tax reporting for everything else.

Transfer pricing has moved from a "document it when audited" exercise to a "document it contemporaneously or face penalties" regime in most major jurisdictions. The BEPS Action 13 framework (Master File, Local File, Country-by-Country Report) is now the baseline expectation.

For mid-market companies with cross-border related-party transactions, the practical requirements:

Master File. A high-level overview of the group's global business, transfer pricing policies, and allocation of income and economic activity. Prepared centrally.

Local File. Detailed transactional documentation for each entity's material related-party transactions, demonstrating arm's-length pricing. Prepared locally, often with central coordination.

Country-by-Country Report (CbCR). Revenue, profit, tax paid, employees, and assets by jurisdiction. Required for groups above the CbCR revenue threshold (typically EUR 750 million, but some jurisdictions have lower thresholds).

The operational challenge for mid-market companies: the data for transfer pricing documentation lives across the ERP (intercompany transactions, pricing, cost allocations), the tax function, and legal entity records. When intercompany transactions are tracked manually or through offline reconciliation, producing defensible transfer pricing documentation is expensive and error-prone.

A pattern we see in implementations for multi-country groups: the cleanest approach is automated intercompany transaction tagging at the point of entry, with intercompany reconciliation reports generated monthly rather than at year-end. This reduces the audit risk and the documentation cost simultaneously. Companies that reconcile intercompany balances annually, rather than monthly, consistently underestimate the effort required when transfer pricing documentation is requested.

This is the single most common structural problem in mid-market international accounting, and it sits underneath every other issue in this guide.

The scenario: a group operates across five or ten countries, each with its own accounting system (or worse, a mix of spreadsheets, local ERP installations, and cloud tools). The group finance team consolidates manually, often using Excel, with currency translation and intercompany elimination done offline. The process takes a week or more at each close. The results are hard to audit and harder to trust.

The 2026 dimension: the regulatory changes above (IFRS 18, Pillar Two readiness, transfer pricing documentation) all assume that the group can produce consolidated, jurisdiction-level financial data quickly and accurately. A manual consolidation process that barely survived the old requirements will not survive the new ones.

A pattern we see across multi-subsidiary implementations: a 9-subsidiary group moving from disconnected local systems to a single cloud ERP with automated journal import, intercompany tagging, and automated elimination reduced its monthly close from over two weeks to under five days. The consolidation was no longer a project. It was a process. The CFO got constant-currency and nominal-currency views of the same data without rebuilding reports.

The operational architecture that works: a centralized cloud ERP for the group (NetSuite OneWorld, or a comparable multi-entity platform), with full transactional depth in the primary operating country and standardized journal import from other countries. Intercompany transactions are tagged at entry. Elimination entries are automated. Consolidated financial statements are generated in both constant and nominal currency. The audit trail runs from the consolidated report all the way down to the source transaction in any subsidiary.

For the detailed mechanics of how this architecture works, see NetSuite OneWorld: Multi-Entity and Multi-Currency ERP Guide. For data migration planning when moving from disconnected systems to a unified platform, see NetSuite Data Migration: Complete Guide for First-Time Buyers.

The five issues in this guide are not independent of each other. Multi-currency revaluation, IFRS 18 presentation, Pillar Two readiness, transfer pricing documentation, and data consolidation all converge on the same underlying requirement: a finance architecture that can produce accurate, jurisdiction-level, auditable data on a close cycle that is measured in days, not weeks.

For mid-market CFOs who already have that architecture in place, the 2026 regulatory changes are manageable configuration adjustments. For those still consolidating manually across disconnected systems, they represent a structural challenge that compounds with every new regulatory requirement.

The practical starting point is an honest assessment of where your current architecture sits. If your close takes more than a week, if your intercompany reconciliation is manual, if your chart of accounts would need a rebuild to produce IFRS 18 subtotals, or if your transfer pricing documentation is assembled retroactively, the cost of inaction is growing.

Softype has implemented multi-subsidiary, multi-currency finance architectures on NetSuite for groups operating across Asia, Africa, the Americas, and Europe. If the issues in this guide are on your CFO agenda, we are happy to walk through the architecture options with you. Reach out at softype.com/contact-us.

Multi-currency revaluation under elevated exchange rate volatility, IFRS 18 income statement presentation changes (effective January 1, 2027), BEPS 2.0 Pillar Two global minimum tax rollout, tightened transfer pricing documentation requirements under BEPS Action 13, and the persistent challenge of consolidating financial data across disconnected subsidiary systems.

IFRS 18 Presentation and Disclosure in Financial Statements was issued by the IASB in April 2024. It replaces IAS 1 and introduces mandatory subtotals in the income statement (operating profit and profit before financing and income taxes), new disclosure requirements for management-defined performance measures, and changes to income and expense classification. It is effective for annual reporting periods beginning on or after January 1, 2027, with early adoption permitted. Comparative restatement is required.

Pillar Two directly applies to groups with consolidated revenue above EUR 750 million. Most mid-market companies fall below this threshold. However, mid-market subsidiaries of larger groups may be in scope, and jurisdictions enacting Pillar Two are also tightening related domestic tax rules. The indirect effects on transfer pricing scrutiny and incentive eligibility may affect mid-market companies even if Pillar Two itself does not.

Multi-currency revaluation restates foreign-currency-denominated balances (receivables, payables, bank accounts, intercompany balances) at the period-end exchange rate. Unrealized gains and losses are recognized in the income statement. In a cloud ERP like NetSuite, revaluation runs automatically at period-end using a configured exchange rate source, posting to designated unrealized foreign exchange gain/loss accounts. Realized gains and losses are recognized separately at the point of settlement.

Transfer pricing documentation demonstrates that related-party cross-border transactions are priced at arm's length. The BEPS Action 13 framework requires a Master File (group overview), a Local File (entity-level transactional detail), and a Country-by-Country Report for groups above the revenue threshold. Most OECD and G20 jurisdictions now require some form of contemporaneous transfer pricing documentation. If your group has material intercompany transactions across borders, you should assume documentation is required.

Best practice for a well-architected multi-subsidiary close is three to five business days. Groups operating on disconnected systems typically take two to four weeks. The difference is almost entirely a function of the consolidation architecture: automated journal import, intercompany tagging, and automated elimination versus manual Excel consolidation.

Yes. Modern cloud ERPs support multi-book accounting, which allows a single transaction to post under multiple accounting standards simultaneously. This means a subsidiary can maintain local GAAP books while the group consolidation runs on IFRS, without duplicate data entry. The chart of accounts and reporting logic need to be designed for both standards from the outset.

This guide covers the 2026 regulatory landscape and the five issues international accounting teams are navigating now. It is written for CFOs evaluating whether their current finance architecture is fit for purpose. The OneWorld guide covers how multi-entity, multi-currency consolidation works technically in NetSuite, including the mechanics of subsidiary setup, intercompany elimination, and currency revaluation. Use this guide for the "what and why." Use the OneWorld guide for the "how."

Helping businesses thrive with integrated ERP solutions.

NetSuite

Service

Company

Contact Us

Copyright © 2026